Budget Model Enhancement FAQ

- What is Responsibility Center Management, or RCM, and how does it work?

- Responsibility Center Management (RCM), commonly known as incentive-based budgeting, is a management philosophy designed to align budget allocations with university goals and objectives by decentralizing several components of the University’s budget authority. The goal is to delegate aspects of the University’s operational authority to colleges, divisions, and other units, allowing them to align their goals with the University’s central mission: Teaching, Research and Scholarship, and Service.

These decentralized models result in increased transparency and empower local leadership to make data-driven decisions.

In an incentive-based budget model a framework is created to direct funding to the units generating the revenue, then charges are assessed to cover the unit’s share of centrally borne expenditures like administrative and common service and support.

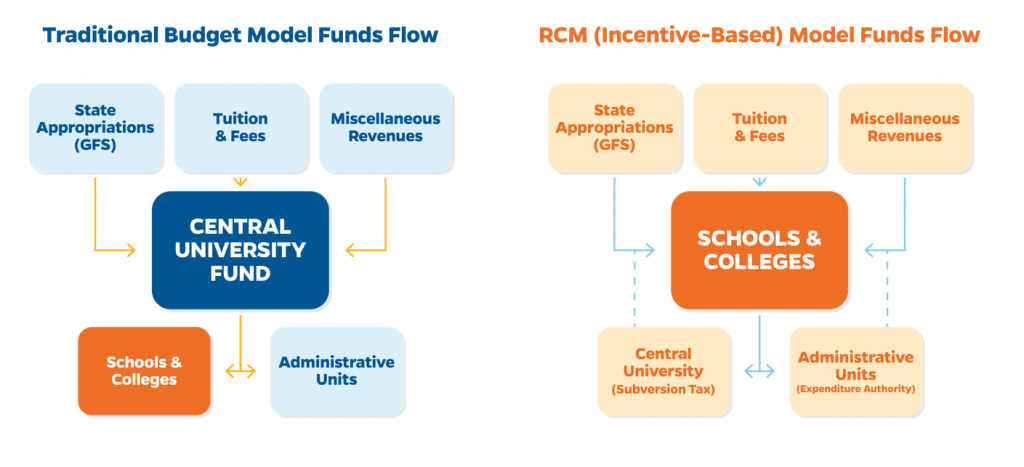

- How do funds flow in an RCM model?

- In RCM models, revenues, based on customized activities or drivers (e.g., credit hours instructed), are allocated directly to the unit generating those activities. Units that do not generate revenues are funded by a overhead allocation fund, which is a determined contribution from each revenue-generating unit to fund University support activities (e.g., IT). An RCM model also leverages a subvention fund which allocates a strategic pool of resources to the University leadership to fund key institutional priorities. It is important to note that in UF’s RCM model, the allocation methodology stops at the school/college level meaning it is the Dean’s discretion as to how funds are allocated within a particular unit.

© 2021 Huron Consulting Group Inc. and affiliates - Why did UF change to an RCM model in 2011?

- At the time, because of the Great Recession, the University was forced to take ongoing expense reductions. This inhibited the university from achieving many of the former President’s Strategic Work Plan goals. Leadership determined that UF “must grow through aggressive management of nontraditional, entrepreneurial growth.” Specifically, UF wanted to make the shift because of:

- Decreasing and uncertain state support

- Increasing self-reliance

- Having the ability to further promote innovative and entrepreneurial activities

that are financially viable - Giving campus units the tools needed to diversify and generate new revenue sources

- Why did UF review and revise the RCM model in 2016? What were the outcomes?

- UF undertook a review of the RCM model in 2016 In an effort to ensure UF’s budgeting process meets the needs of the university. The scope of the review was to identify what was working with the budget model as well as how it might be improved in the areas of revenue and

expense allocation. Specially the goals of this review were to:- Ensure the model was incentivizing the right activities

- Simplify the model

- Increase predictability

- Align model with University strategic goals

- Provide clarity

- Create dedicated Provost strategic fund

The effort resulted in several key enhancements including simplifying allocation methodologies, reducing the complexity of overhead assessments by standardizing model tax rates, the establishment of a Provost strategic fund. The comprehensive report can be found here.

- Why is UF doing another review of the RCM model after just completing one in 2016?

- Modern budget philosophy within higher education continues to evolve much like the industry as a whole. Best-practice has proven that universities who operate within an RCM budgeting framework can benefit from modest modifications to the budget model every 4-5 years. As universities continue to mold to the environments around them, it is important to ensure funding practices are aligned with an institution’s strategic priorities. Further, model mechanics that may have made sense in theory (e.g., step-down costing) may not be feasible in day-to-day practice or may be unnecessarily cumbersome. Thus, convening a thorough review of the budget model on a regular 5-year basis can ensure the model continues to allocate resources appropriately across the institution and ensure long-term model understanding and sustainability.

- What are the intended outcomes of the current review and subsequent enhancements?

- The 2021 review of UF’s Budget Model resulted in over 50 potential enhancement opportunities. Through the engagement’s governance process, those opportunities were narrowed down to 7 near-term enhancements. The intended outcomes of these enhancements are detailed below and are being developed over the course of this academic year.

- How will UF component units be affected by this effort?

- Component units will largely be unaffected by this effort. Specifically, no funding or process changes will occur within component units because of this effort. However, as part of the all-funds enhancement, UF will need to understand the comprehensive financial picture of each component unit to incorporate that view within UF’s all-funds model. Specific leaders of these component units have already been identified and engaged to assist with this ongoing effort. All questions related to component unit funding and other unit-specific operations, should be directed to the leadership team of that component unit.

- The University is implementing a new budget and planning tool to help with the budget development process. How is that related to this effort?

- The University has selected Workday Adaptive Planning as new tool to replace the current Hyperion budget tool. While that effort is not an explicit enhancement coming out this engagement, it is directly tied to the work that is being completed as a part of this effort. The decisions and outcomes made through this process will be incorporated into the new tool’s infrastructure. More details as to the timeline, process, and intended outcomes of this effort will be made available as progress is made. For more information, please visit the Budget Process and System Evaluation section of this website.

- How are model enhancement decisions being made and how is the input of campus being handled?

- There are five primary avenues for campus involvement and input:

- Working Group – The Working Group is charged with leading the modifications to the RCM budget model. The Working Group is made up of a diverse set of campus members from several colleges and roles. One of the jobs of each Working Group member is to solicit feedback from his/her constituents so that their opinions can be considered throughout this engagement.

- Implementation Teams – Each Implementation Team will be directly involved in carrying out each of the previously listed enhancements. These groups are made up of a broad array of campus constituents and each group has at least one member who is an academic dean. Updates from these meetings will be published as needed.

- Deans – Deans are actively involved in this process and are engaged by project leadership on a regular basis. They should be able to provide ongoing updates to their specific colleges as needed as the engagement progresses and may drive change at the local college level.

- Unit Budget Officers – Staring in the late Fall timeframe, the CFO’s office will re-establish a roundtable of unit business officers to discuss engagement updates, provide an avenue for feedback, and outline the necessary steps needed to implement each enhancement.

- Open Forums – In the Spring, the CFO’s office will work to schedule a series of open forums where campus can learn about initiative progress and ask any relevant questions. These campus forums will be either in-person or online and will be recorded and open to all UF employees. More details regarding time and location will be made available closer to the date.

- How can I submit a question about this effort?

- Please submit all questions, comments, and feedback here. We will get back to you as soon as possible.

Intended Outcomes

Enhancement Objective |

Intended Outcome |

| 1. Create an all-funds model | Provide a comprehensive, transparent view into all of the resources, expenses, and commitments that exist across the University and its affiliated component units. |

| 2. Eliminate step-down costing | Simplify the model by eliminating direct overhead costs charged to support units. |

| 3. Build strategy for deferred maintenance | Develop a consistent strategy to fund and address deferred maintenance needs across campus. |

| 4. Review uses of the General Funds Supplement (GFS) | Evaluate the current uses of the GFS and determine potential changes to the allocation methodology to better help achieve institutional priorities. |

| 5. Clarify overhead assessments | Review and re-base (where appropriate) overhead assessments to colleges and auxiliaries to enhance transparency and accuracy of these assessments. |

| 6. Enhance strategic fund transparency | Document and clarify where and how strategic commitments are made across the University. |

| 7. Retool major capital governance | Establish a modified capital planning and approval process and correlated governance structure to plan for, manage, and execute on new capital requests and projects |

Page Contents